Sometimes I wonder if I’m living in the clouds. All of my recent reports on the Canadian dollar were twinged with pessimism, and I argued that it would only be a matter of time before reality caught up with theory. While the continued surge in commodities prices has confounded everyone’s expectations, other economic trends continue to work against Canada. In other words, I think that there is still a strong argument to be made for shorting the loonie.

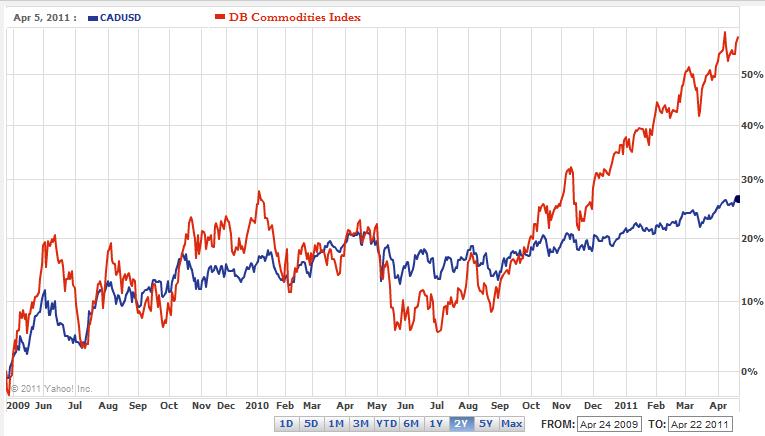

To be sure, the rally in commodities prices has been incredible- nearly 50% in less than a year! Oil prices are surging, gold prices just touched a record high, and a string of natural disasters have driven prices for agricultural staples to stratospheric levels. Given the perception of the Canadian dollar as a commodity currency, then, it’s no wonder that rising commodity prices have translated into a stronger currency.

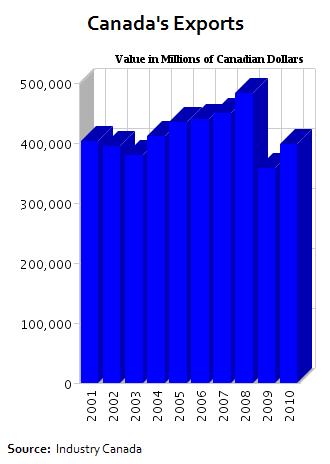

As I’ve argued previously, rising commodities prices are basically an irrelevant – or even distracting – factor when it comes to analyzing the loonie. That’s because, contrary to popular belief, commodities represent an almost negligible component of Canada’s economy. Canadian exports, of which commodities probably account for half, have recovered from the recession lows of 2009. On the other hand, the value of Canadian exports is basically the same as it was 10 years ago, when one US dollar could be exchanged for 1.5 Canadian dollars.

Consider also that Canada now imports more than it exports, and that the Canadian balance of trade recently dipped into deficit for the first time since records started being kept 40 years ago. Its current account has similarly plunged, as Canadians have had to finance this through loans and investment capital from abroad. Based on the expenditure approach to GDP, trade actually detracts from Canadian GDP. Any way you perform the calculations, commodities are hardly the backbone of its economy, account for about 15% at most.

Consider also that Canada now imports more than it exports, and that the Canadian balance of trade recently dipped into deficit for the first time since records started being kept 40 years ago. Its current account has similarly plunged, as Canadians have had to finance this through loans and investment capital from abroad. Based on the expenditure approach to GDP, trade actually detracts from Canadian GDP. Any way you perform the calculations, commodities are hardly the backbone of its economy, account for about 15% at most.

As if that weren’t enough, the press is full of stories of Canadians that think their own currency is overvalued. Businesses complain that they can’t compete, and that banks won’t lend them the money they need to upgrade their facilities and become more efficient. Meanwhile consumers whine about higher prices in Canada, compared to the US. I think it’s very telling that there is now a 2-hour wait to cross the border from Vancouver, and shopping malls on the American side have reported a huge jump in business. Even the famous Big Mac Index shows that the price of a hamburger was already 12% higher in Canada back when the loonie was still hovering around parity with the US Dollar.

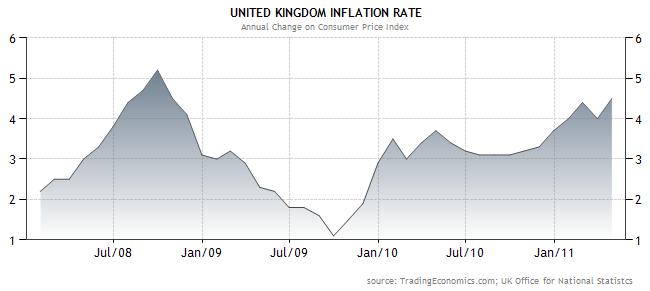

One area that higher commodities prices will be felt is inflation, which is nearing a two-year high and rising. At 3.3%, Canada’s CPI rate is now higher than in the EU. Given that the European Central Bank hiked rates earlier this month, it probably won’t be long before the Bank of Canada follows suit. In fact, forecasters expect the benchmark rate to rise by 50-75 basis points by the end of the year, from the current 1%.

As if that weren’t enough, the press is full of stories of Canadians that think their own currency is overvalued. Businesses complain that they can’t compete, and that banks won’t lend them the money they need to upgrade their facilities and become more efficient. Meanwhile consumers whine about higher prices in Canada, compared to the US. I think it’s very telling that there is now a 2-hour wait to cross the border from Vancouver, and shopping malls on the American side have reported a huge jump in business. Even the famous Big Mac Index shows that the price of a hamburger was already 12% higher in Canada back when the loonie was still hovering around parity with the US Dollar.

One area that higher commodities prices will be felt is inflation, which is nearing a two-year high and rising. At 3.3%, Canada’s CPI rate is now higher than in the EU. Given that the European Central Bank hiked rates earlier this month, it probably won’t be long before the Bank of Canada follows suit. In fact, forecasters expect the benchmark rate to rise by 50-75 basis points by the end of the year, from the current 1%.

This might excite carry traders, but probably few others. Besides, given that other central banks will probably raise rates concurrently, it can’t be assumed that carry traders will automatically gravitate towards the Canadian dollar. Not to mention that as I pointed out in my previous post, the carry trade is hardly a risk-free proposition. In this case, an interest rate differential of only 1-2% probably isn’t enough to compensate for the risk of a correction in the USD/CAD.

This might excite carry traders, but probably few others. Besides, given that other central banks will probably raise rates concurrently, it can’t be assumed that carry traders will automatically gravitate towards the Canadian dollar. Not to mention that as I pointed out in my previous post, the carry trade is hardly a risk-free proposition. In this case, an interest rate differential of only 1-2% probably isn’t enough to compensate for the risk of a correction in the USD/CAD.

And that is exactly what I expect will happen. The fact that the loonie has shattered even the most optimistic forecasts is not cause for bullishness, but rather for concern. According to the most recent Commitment of Traders report, net long positions are reaching extreme levels, and it’s probably only a matter of time before the loonie returns to earth.

To be sure, the rally in commodities prices has been incredible- nearly 50% in less than a year! Oil prices are surging, gold prices just touched a record high, and a string of natural disasters have driven prices for agricultural staples to stratospheric levels. Given the perception of the Canadian dollar as a commodity currency, then, it’s no wonder that rising commodity prices have translated into a stronger currency.

As I’ve argued previously, rising commodities prices are basically an irrelevant – or even distracting – factor when it comes to analyzing the loonie. That’s because, contrary to popular belief, commodities represent an almost negligible component of Canada’s economy. Canadian exports, of which commodities probably account for half, have recovered from the recession lows of 2009. On the other hand, the value of Canadian exports is basically the same as it was 10 years ago, when one US dollar could be exchanged for 1.5 Canadian dollars.

Consider also that Canada now imports more than it exports, and that the Canadian balance of trade recently dipped into deficit for the first time since records started being kept 40 years ago. Its current account has similarly plunged, as Canadians have had to finance this through loans and investment capital from abroad. Based on the expenditure approach to GDP, trade actually detracts from Canadian GDP. Any way you perform the calculations, commodities are hardly the backbone of its economy, account for about 15% at most.

Consider also that Canada now imports more than it exports, and that the Canadian balance of trade recently dipped into deficit for the first time since records started being kept 40 years ago. Its current account has similarly plunged, as Canadians have had to finance this through loans and investment capital from abroad. Based on the expenditure approach to GDP, trade actually detracts from Canadian GDP. Any way you perform the calculations, commodities are hardly the backbone of its economy, account for about 15% at most. As if that weren’t enough, the press is full of stories of Canadians that think their own currency is overvalued. Businesses complain that they can’t compete, and that banks won’t lend them the money they need to upgrade their facilities and become more efficient. Meanwhile consumers whine about higher prices in Canada, compared to the US. I think it’s very telling that there is now a 2-hour wait to cross the border from Vancouver, and shopping malls on the American side have reported a huge jump in business. Even the famous Big Mac Index shows that the price of a hamburger was already 12% higher in Canada back when the loonie was still hovering around parity with the US Dollar.

As if that weren’t enough, the press is full of stories of Canadians that think their own currency is overvalued. Businesses complain that they can’t compete, and that banks won’t lend them the money they need to upgrade their facilities and become more efficient. Meanwhile consumers whine about higher prices in Canada, compared to the US. I think it’s very telling that there is now a 2-hour wait to cross the border from Vancouver, and shopping malls on the American side have reported a huge jump in business. Even the famous Big Mac Index shows that the price of a hamburger was already 12% higher in Canada back when the loonie was still hovering around parity with the US Dollar.

And that is exactly what I expect will happen. The fact that the loonie has shattered even the most optimistic forecasts is not cause for bullishness, but rather for concern. According to the most recent Commitment of Traders report, net long positions are reaching extreme levels, and it’s probably only a matter of time before the loonie returns to earth.

Read more

{kind=link}

{kind=link}

{kind=link}